If you work from home in India—whether for a local corporate hub or an overseas tech client—your tax structure changed drastically this year. Thanks to the enhanced New Tax Regime, an income up to ₹12 Lakhs can now be effectively tax-free under Section 87A.

Thank you for reading this post, don't forget to subscribe!How you maximize your savings depends entirely on your legal status. Here is your ultimate tax-saving playbook for the year.

A: You are a Freelancer or Independent Contractor

If you receive gross payouts without a Form 16, you are classified under Profits and Gains from Business or Profession (PGBP). You have the best tax-saving toolkit available.

1. The 50% Rule: Presumptive Taxation (Section 44ADA)

If your gross annual earnings are up to ₹75 Lakhs, you don’t need to track every single receipt.

- The Magic: The government presumes 50% of your income goes toward expenses. You are only taxed on the remaining 50%.

- The “Zero Tax” Hack: If you make ₹22 Lakhs, your taxable income drops to ₹11 Lakhs under Section 44ADA. Because that falls below the New Tax Regime’s ₹12 Lakh threshold, your net tax liability drops to ₹0.

Read More….Tax Saving Tips for Remote Workers in India (2026-27): Save Thousands Easily!

2. Itemized Deductions (If Gross Receipts Cross ₹75 Lakhs)

If you exceed the presumptive limit, you can deduct every single cost required to keep your remote office running:

- Tech & Gadgets: You can claim annual depreciation (40% for computers/software) on laptops, tablets, and ergonomics.

- Subscriptions: 100% of your SaaS bills (Slack, Notion, Figma, GitHub, AWS/Azure, Adobe).

- Workspace & Bills: A proportionate slice of your home rent, electricity, and monthly broadband bills.

- Client Acquisition: Cabs, flights, and meals used to pitch or retain clients.

B: You are a Salaried Remote Employee

If you are on a fixed corporate payroll, your deductions depend entirely on which tax regime you select.

1: The New Tax Regime (The Default)

- Standard Deduction: Now bumped up to ₹75,000—deducted automatically with zero paperwork.

- Corporate NPS (Sec 80CCD(2)): Up to 10% of your basic salary is tax-deductible if your company co-contributes to your National Pension System.

2: The Old Tax Regime (Must Opt-In)

If you actively choose to opt out of the new system, ensure your HR structures your CTC to include:

- Internet Reimbursements: Under Rule 3(7)(ix), actual monthly Wi-Fi bill reimbursements from your employer are 100% tax-free.

- HRA (House Rent Allowance): Fully claimable even if you work from a hometown tier-2 city, provided you have a formal rent agreement (even with parents).

- Skill Allowances: Tax-free allocations for journals, research materials, or digital courses.

The Compliance Checklist

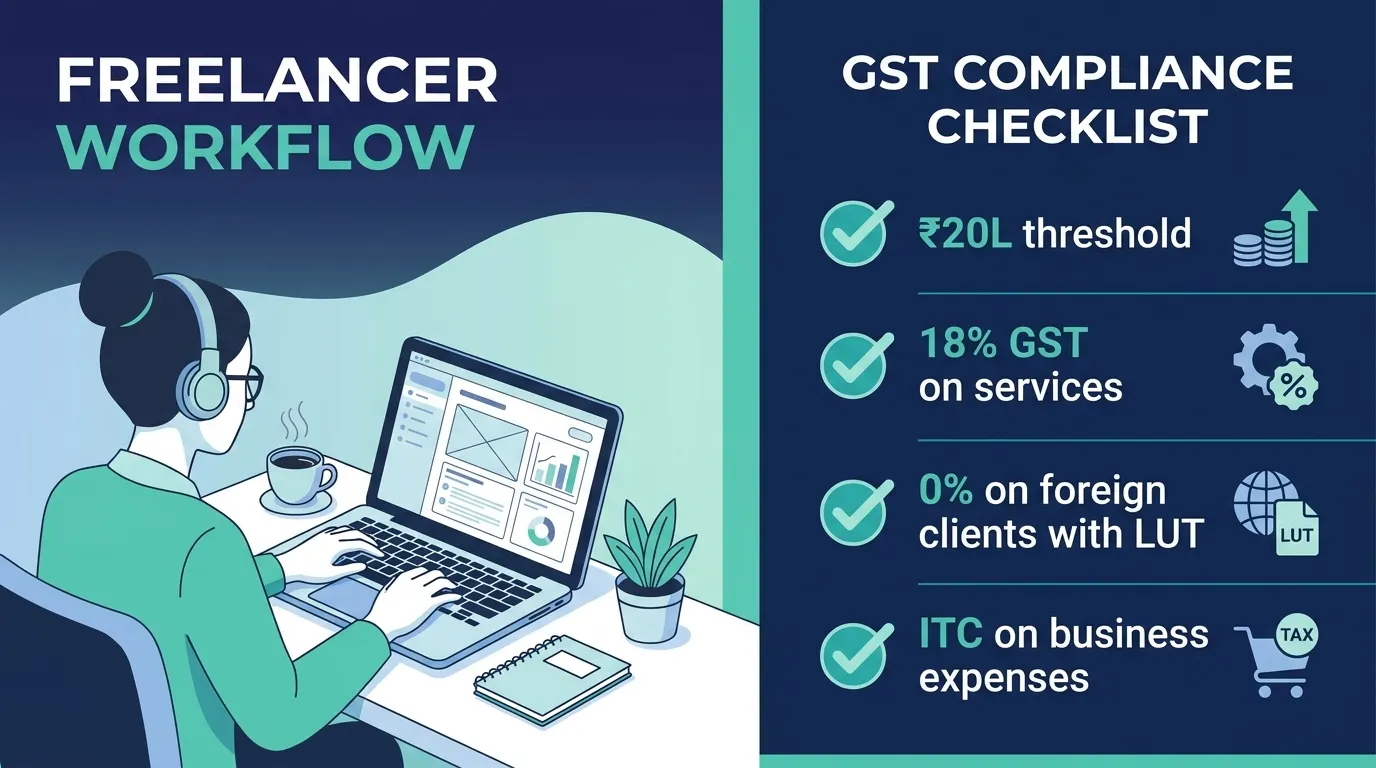

- GST Warning: If your freelance revenue crosses ₹20 Lakhs, GST registration is mandatory. Even if you export services to US/EU clients at a 0% tax rate, you must file a Letter of Undertaking (LUT).

- Advance Tax: If your net freelance tax liability exceeds ₹10,000, you must pay your taxes in quarterly installments (June, September, December, March) to avoid interest penalties.

No, not directly as deductions. If you are a salaried employee, you cannot write off actual utility bills or asset depreciation on your tax return. However, there are two ways to optimize this:

Under the New Tax Regime: You receive a flat, automatic Standard Deduction of ₹75,000, which is designed to cover general employment-related costs without requiring you to submit any bills.

Under the Old Tax Regime: You can save tax on these expenses only if your employer structures them as reimbursements (e.g., Internet/Telephone Reimbursement under Rule 3(7)(ix)) instead of a fixed allowance. Reimbursements against actual bills are 100% tax-free.

No. Section 44ADA is an “all-inclusive” scheme. When you opt for it, the Income Tax Department automatically assumes that 50% of your gross receipts went toward running your profession (which covers your rent, Wi-Fi, gadgets, software licenses, and travel).

Because of this generous 50% flat deduction, you cannot claim any individual business expenses or laptop depreciation on top of it. If your actual expenses are higher than 50%, you must skip Section 44ADA and file under the regular ITR-3 form with fully audited books of accounts.

Yes, registration may be required, but your effective tax rate will likely be 0%.

The Threshold: If your total gross turnover across all clients (domestic and international) crosses ₹20 Lakhs (₹10 Lakhs in northeastern states), you must register for GST.

The Zero-Rated Advantage: Providing remote services to a client outside India is legally classified as an “Export of Services.” Under GST laws, exports are considered “zero-rated supplies.” This means you do not have to charge any GST to your foreign client, provided you file a Letter of Undertaking (LUT) on the GST portal at the beginning of the financial year.

"Suresh Kumar Saini is an experienced Tax Assistant and finance writer. He specializes in US & Canada Tax Guide, Indian Income Tax laws, GST compliance, and personal finance, helping freelancers and remote workers optimize their taxes."