Tax season can feel like a moving target, and the 2026 tax brackets are no exception. Every year, the IRS adjusts tax thresholds to combat “bracket creep”—a phenomenon where inflation bumps you into a higher tax tier even if your actual purchasing power hasn’t changed.

Thank you for reading this post, don't forget to subscribe!While the seven core federal income tax rates remain steady at 10%, 12%, 22%, 24%, 32%, 35%, and 37%, the income ranges themselves have shifted upward. This means you can earn a bit more money before stepping into a higher tax bracket.

Here is exactly how the 2026 brackets and deductions shake out, and what it actually means for your money.

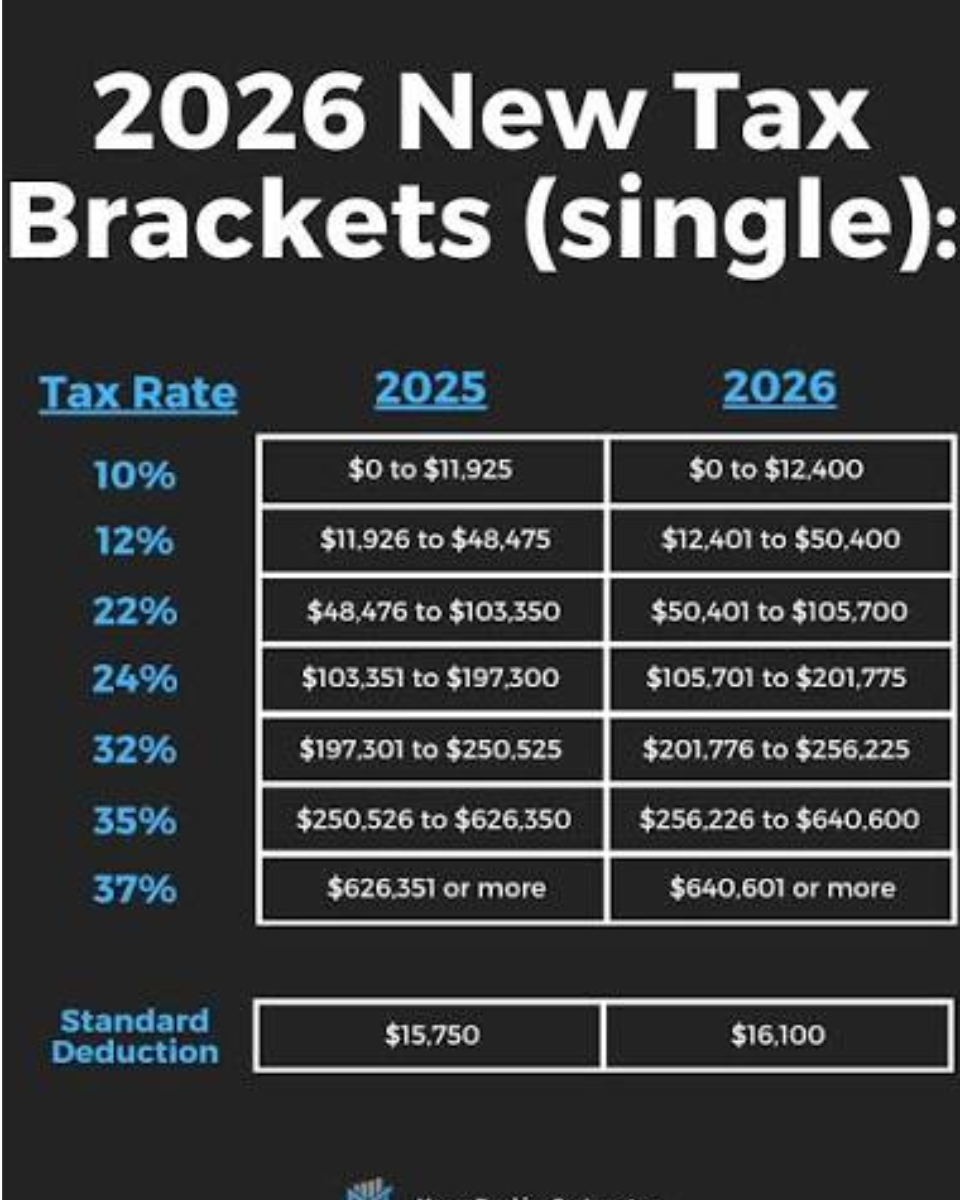

The 2026 Income Tax Brackets

A quick reminder on how the U.S. progressive tax system works: You aren’t taxed at one flat rate for your entire income. Instead, your income is taxed in “chunks.” If you land in the 22% bracket, only the dollars above that specific threshold are taxed at 22%; the money below it is still taxed at the lower 10% and 12% rates.

For Single Filers

| Tax Rate | 2026 Taxable Income Range |

| 10% | $0 to $12,400 |

| 12% | $12,401 to $50,400 |

| 22% | $50,401 to $105,700 |

| 24% | $105,701 to $201,775 |

| 32% | $201,776 to $256,225 |

| 35% | $256,226 to $640,600 |

| 37% | Over $640,600 |

For Married Couples Filing Jointly

| Tax Rate | 2026 Taxable Income Range |

| 10% | $0 to $24,800 |

| 12% | $24,801 to $100,800 |

| 22% | $100,801 to $211,400 |

| 24% | $211,401 to $403,550 |

| 32% | $403,551 to $512,450 |

| 35% | $512,451 to $768,700 |

| 37% | Over $768,700 |

The Higher Standard Deductions

Before those tax brackets even touch your income, the standard deduction lowers your taxable base. For 2026, standard deductions have been bumped up across the board:

- Single / Married Filing Separately: $16,100 (up $350 from 2025)

- Married Filing Jointly: $32,200 (up $700 from 2025)

- Head of Household: $24,150 (up $525 from 2025)

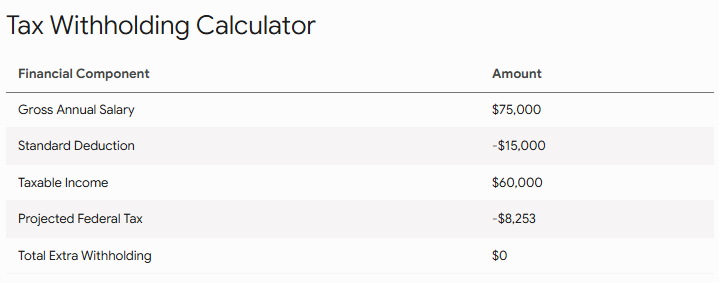

What this means for you: If you are a single filer making $60,000, your first $16,100 is completely tax-free. Your taxable income drops to $43,900, placing your highest dollar safely in the 12% bracket rather than the 22% bracket.

3 Ways This Directly Affects Your Paycheck

The shift in brackets has a tangible, ripple effect on everyday financial decisions. Here is where you will notice it most:

1. Protection Against “Bracket Creep”

If you received a modest raise recently to match the rising cost of living, these adjusted brackets help ensure that your raise won’t be immediately swallowed up by a higher tax tier. You keep a slightly larger percentage of your hard-earned money.

2. Room to Save More (Pre-Tax)

The IRS has also increased the contribution limits for major retirement and health savings accounts. If you want to deliberately push your taxable income into a lower bracket, you can stash more money away pre-tax:

- 401(k) limits have increased to $24,500 (with an $8,000 catch-up limit for those 50+).

- Traditional and Roth IRA limits have ticked up to $7,500.

- Health Savings Accounts (HSAs) limits are up to $4,400 for individuals and $8,750 for families.

3. Key Deductions and Breaks

Recent adjustments keep specific, helpful breaks intact. Notably, there are enhanced write-offs for qualifying overtime pay and tips (up to specific income limits), alongside an expanded senior deduction of up to $6,000 for taxpayers aged 65 and older who meet the income thresholds. Non-itemizers can also deduct cash donations up to $1,000 (single) or $2,000 (married joint).

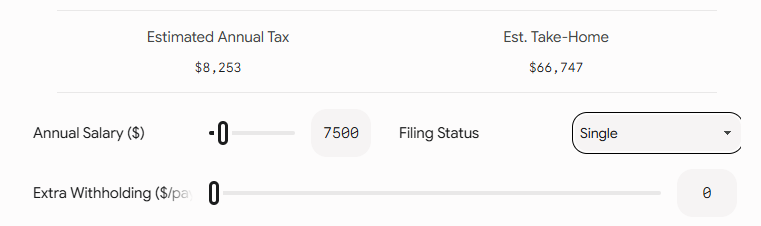

See How the Brackets Impact Your Specific Income

To help you visualize exactly how your income gets divided into these brackets and estimate your final tax liability, you can plug your numbers into the interactive calculator below.

Editing by- katie willimas

Suresh Kumar Saini is a financial analyst and tax consultant specializing in US taxation, IRS guidelines, and banking services. With years of research in global finance, he helps readers simplify complex credit card rewards and financial laws.