For high-income earners in Canada, choosing between an RRSP and a TFSA isn’t an “either/or” debate—it’s a sequence. While both accounts offer tax-sheltered growth, the RRSP (Registered Retirement Savings Plan) is almost always the mathematically superior account to prioritize first.

Thank you for reading this post, don't forget to subscribe!The strategy comes down to a simple formula: Max the RRSP for immediate relief, then use the tax savings to fund the TFSA.

Why the RRSP Wins When Income is High

The true value of an RRSP relies on tax arbitrage: Your marginal tax rate today vs. your expected tax rate in retirement.

Because your current income puts you in a top tax bracket, the math swings heavily in favor of the RRSP:

- The Immediate Deduction: RRSP contributions use pre-tax dollars. If your marginal tax rate is $45%, a $10,000 contribution slashes your current tax bill by $4,500.

- The Retirement Arbitrage: You will pay tax when you withdraw this money in retirement. However, most people have significantly lower income in retirement than during their peak earning years. If your retirement tax bracket drops to $25%, you effectively bypassed a $45% tax rate today to pay only $25% later.

When the TFSA Takes the Lead

Even with a high income, you should prioritize your TFSA (Tax-Free Savings Account) if any of these exceptions apply to you:

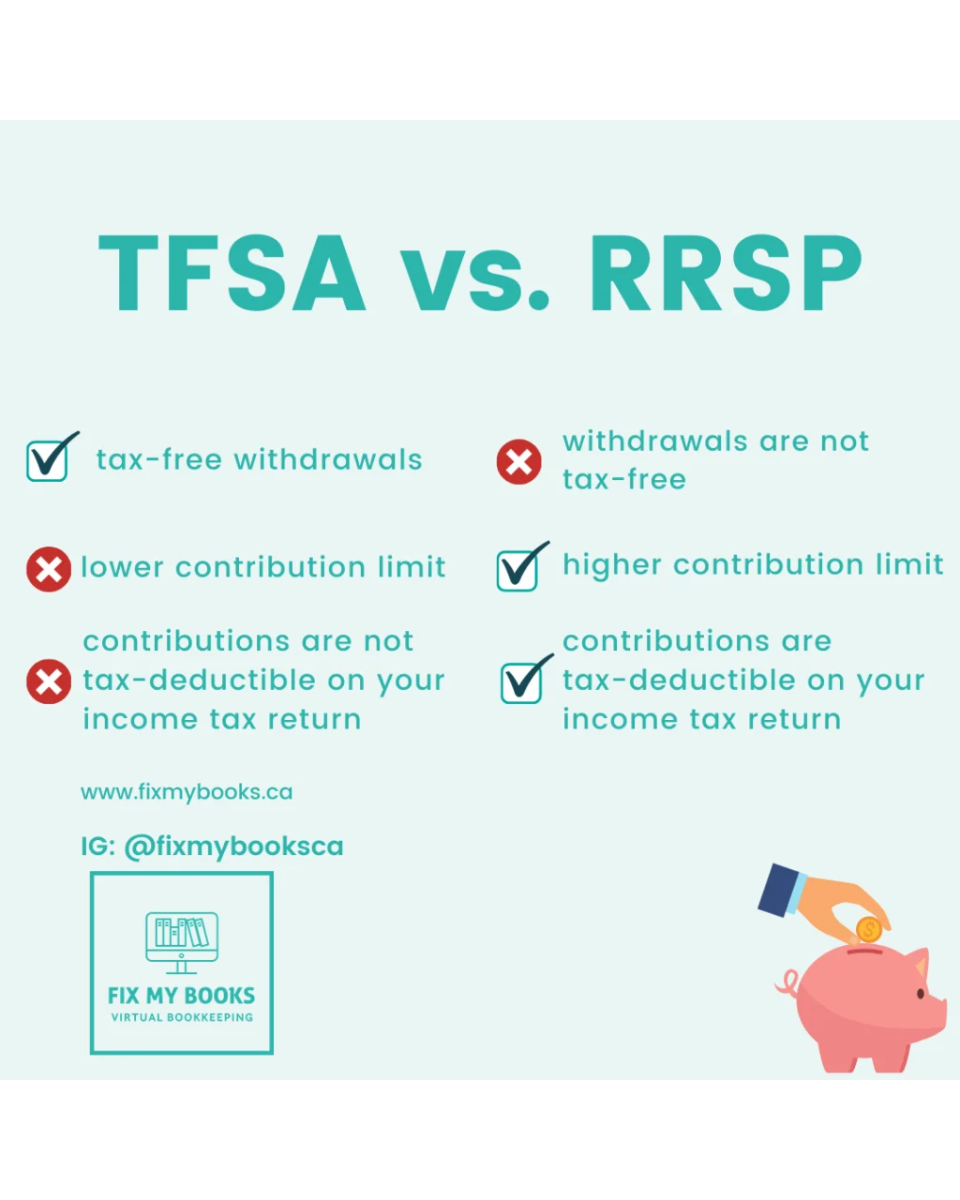

- You need near-term flexibility: RRSP withdrawals are immediately hit with withholding taxes, and you permanently lose that contribution room. TFSA withdrawals are $100% tax-free, and you get the contribution room back the very next year.

- You are a U.S. citizen: The IRS does not recognize the tax-free status of a TFSA, resulting in complex U.S. tax reporting obligations. The RRSP is fully recognized under the Canada-U.S. tax treaty.

- You expect a massive retirement income: If a corporate pension, real estate portfolio, or non-registered investments will keep you in a top tax bracket during retirement, the RRSP’s tax arbitrage disappears.

Read More….RRSP vs TFSA for Canadian Expats & Freelancers

The Power Strategy: The Financial Feedback Loop

If your cash flow allows, the ultimate high-earner strategy is to loop these accounts together to let the government fund your savings:

[High Income Salary] ──> [Contribute to RRSP] ──> [Generates Large Tax Refund]

│

▼

[Max out remaining RRSP/TFSA room] <── [Reinvest Refund into TFSA]

- Max your RRSP to trigger the largest possible tax deduction.

- Take the tax refund generated by that deduction.

- Immediately deposit that refund into your TFSA.

By using this loop, you are effectively turning your immediate tax savings into tax-free compounding growth. Once both vehicles are entirely maxed out, you can then pivot your surplus cash toward non-registered taxable accounts.

Editing by-katie willimas

Suresh Kumar Saini is a financial researcher specializing in US Personal Finance, Online Banking, and US Tax Guides, helping individuals navigate complex financial systems.