A quick macro-driven pop has crypto green this morning, but the actual headline you should be watching is a quiet policy shift that could fundamentally change how you buy your next home.

Thank you for reading this post, don't forget to subscribe!Here is the breakdown of today’s market numbers, what they mean for your purchasing power, and how the rules are about to change for home buyers.

The Morning Snapshot

Bitcoin and Ethereum both notched 3% gains this morning following claims from President Trump that the conflict in Iran has concluded. However, investors are preaching caution; similar false alarms over the past month mean the market remains highly volatile.

Even with this morning’s bounce, both major assets are trading at massive discounts relative to their 2025 peaks:

| Crypto Asset | Price This Morning (June 12, 2026) | Morning Move | Distance From All-Time High |

| Bitcoin (BTC) | $63,718.04 | Up 3.4% | -49.5% (ATH: $126,198.07 in Oct 2025) |

| Ethereum (ETH) | $1,671.54 | Up 3.2% | -66.3% (ATH: $4,953.73 in Aug 2025) |

Turning Digital Wealth into Real Estate

If you have a digital nest egg, can you actually use it to bypass a traditional mortgage or secure a front door?

Historically, the answer was a headache. To use crypto for a down payment, lenders required you to sell it, convert it to US dollars, and let it sit in a traditional bank account for 60 days to “season.” The immediate downside? Massive capital gains taxes that instantly ate into your purchasing power.

But a massive structural upgrade is underway.

“I want people who own cryptocurrency to be able to buy homes like everyone else… It’s time the housing system caught up.”

— William J. Pulte, FHFA Director

In a direct bid to position the U.S. as the “crypto capital of the world,” the Federal Housing Finance Agency (FHFA) has officially ordered underwriting giants Fannie Mae and Freddie Mac to prepare their systems to recognize cryptocurrency as a valid asset for qualifying for a mortgage.

What Changes for You?

Once these guidelines roll out to local lenders, you will no longer be forced to panic-sell your tokens just to pass a mortgage background check. Traditional banks will eventually evaluate your crypto holdings the same way they look at a 401(k), mutual fund, or stock portfolio when approving a loan.

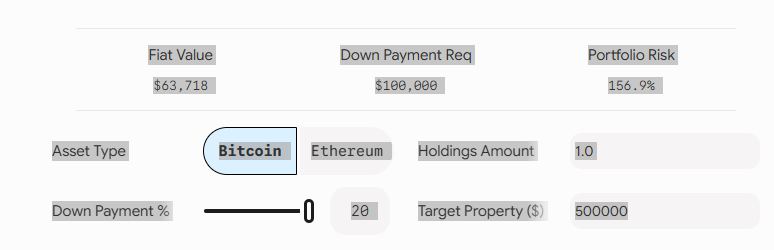

To see how your specific portfolio balances translate into purchasing power or down payment collateral under different market conditions, test your numbers below:

Crypto Purchasing Power Evaluator

Editing by- katie willimase

Suresh Kumar Saini is a financial analyst and tax consultant specializing in US taxation, IRS guidelines, and banking services. With years of research in global finance, he helps readers simplify complex credit card rewards and financial laws.