The GST Council has introduced a significant, taxpayer-friendly reform to the Annual Return Form GSTR-9 for the Financial Year (FY) 2024–25. This change addresses a long-standing point of confusion and a frequent trigger for tax notices: the reporting of delayed Input Tax Credit (ITC).

Thank you for reading this post, don't forget to subscribe!

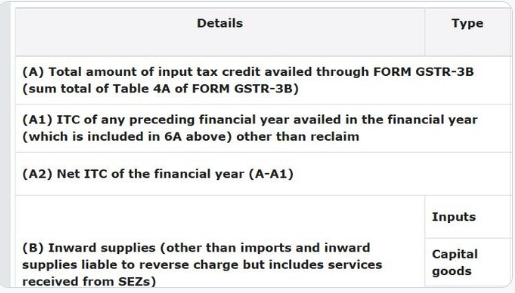

For FY 2024–25, taxpayers filing GSTR-9 (not GSTR-9A for Composition taxpayers) must use the new Table 6A1.

This dedicated field is designed to clearly report ITC that belongs to the previous financial year (FY 2023–24) but was actually claimed in the current year’s GSTR-3B returns (filed between April and October 2024, up to the November 30th deadline).

Why This Matters: Before this change, there was no clear place to report these “carry-forward” ITC claims, often forcing taxpayers to use generic tables or enter negative values. This lack of clarity frequently resulted in mismatches between GSTR-3B and GSTR-9, leading to departmental scrutiny and unnecessary litigation.

The introduction of Table 6A1 is expected to:

Enhance Transparency: Provide a clear, reconciled view of cross-year ITC adjustments.

Reduce Notices: Minimize discrepancies that typically trigger tax authority queries.

Simplify Audits: Allow tax officers to easily verify ITC claims between financial years.

The Crucial Step Taxpayers Must Watch

While Table 6A1 brings clarity, taxpayers cannot afford to relax on their record-keeping. Tax professionals caution that the department will use this structured data to perform direct verification checks.

Taxpayers must ensure perfect consistency between the ITC reported in:

Table 6A1 of the current year’s GSTR-9 (for FY 2024–25).

Table 12 (ITC reversal) and Table 13 (ITC availed) of the previous year’s GSTR-9 (for FY 2023–24).

This cross-verification is intended to confirm that any delayed claim being reported in Table 6A1 was, in fact, an unclaimed or reversed credit from the prior year.

Preparing for the Deadline

The GSTR-9 for FY 2024–25 is currently live on the GST portal, with a filing deadline of December 31, 2025.

Businesses should start performing detailed ITC reconciliations now. Maintaining accurate working papers and robust supporting documentation is essential to smoothly transition to this new, more granular reporting requirement and avoid any discrepancies that could invite departmental queries.