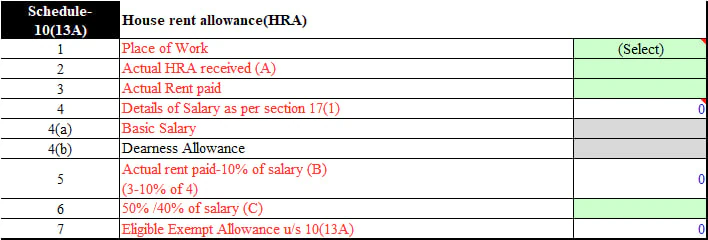

A significant “glitch” in the Income Tax Return (ITR) utility for Financial Year (FY) 2024–25 is causing concern among salaried taxpayers regarding their House Rent Allowance (HRA) claims. Chartered Accountant Himank Singla has warned that the ITR portal incorrectly prompts users to enter their “Place of Work” instead of their “Place of Residence” for HRA exemption calculation under Section 10(13A).

Thank you for reading this post, don't forget to subscribe!

Key Issues and Implications:

- Incorrect City Selection: The Income Tax Act bases HRA exemption on the taxpayer’s residential city (50% of salary for metro cities, 40% for non-metro cities). The ITR utility’s prompt for “Place of Work” directly contradicts this rule.

- Over/Underclaiming HRA: This flaw could lead to taxpayers either claiming more HRA than they are eligible for (if they work in a metro city but reside in a non-metro) or less (if they reside in a metro city but work in a non-metro).

- Compliance Risks: Such discrepancies may trigger scrutiny from the Income Tax Department or result in defective return notices, requiring taxpayers to justify their claims.

- Urgent Rectification Needed: Singla has urged the Income Tax Department to fix this issue immediately to prevent widespread filing errors as the deadline for ITR filing approaches. He advises taxpayers to manually override the portal’s suggestion and calculate their exemption based on their actual residence until the utility is corrected.

Understanding HRA Exemption under Section 10(13A):

HRA is a component of a salaried employee’s income designed to help cover rental expenses. It is generally taxable, but partial or full exemption can be claimed under Section 10(13A) under the old tax regime only. No HRA exemption is allowed if:

- The taxpayer lives in their own house.

- The taxpayer opts for the new tax regime.

Calculation of Exempt HRA:

The exempt amount is the least of the following three:

- Actual HRA received.

- 50% of salary (for metro cities: Delhi, Mumbai, Kolkata, Chennai) or 40% of salary (for non-metro cities).

- Rent paid minus 10% of salary.

- Salary for HRA purposes: Includes basic pay, dearness allowance (if it forms part of retirement benefits), and commission (if based on turnover).

Conditions for Claiming HRA Exemption:

- Must be a salaried individual receiving HRA.

- Must live in rented accommodation.

- Must maintain valid rent receipts and proof of rent payments.

- If annual rent exceeds Rs 1 lakh, the landlord’s PAN is mandatory. If the landlord does not have a PAN, a self-declaration from the landlord stating this, along with their name and address, is required as per CBDT Circular No. 8/2013 dated October 10, 2013.

Documents Required (for employer verification and departmental inquiries, not for filing with ITR):

- Rent receipts for the applicable financial year.

- Rental agreement as proof of tenancy.

- Form 12BB (to declare HRA claim to employer).

- Bank statement or payment proof showing rent transfers.

- Salary slip reflecting the HRA component.

- Landlord’s PAN (if annual rent exceeds Rs 1 lakh), or a self-declaration if the landlord doesn’t have a PAN.

Current Status of the Glitch:

While the Income Tax Department’s e-filing portal has undergone updates and various common issues have been addressed, there is no official confirmation yet regarding the specific “Place of Work” vs. “Place of Residence” glitch for HRA calculation in the FY 2024-25 ITR utility. Taxpayers are advised to exercise caution and follow the guidance of tax experts like CA Himank Singla, who recommend manually calculating and overriding the portal’s suggestion if it presents the incorrect prompt.

For assistance with ITR utility issues, taxpayers can contact the Income Tax Department’s e-filing and Centralized Processing Center helpdesks at:

- Toll-free numbers: 1800 103 0025, 1800 419 0025

- Helpline numbers: +91-80-46122000, +91-80-61464700

- Email: ITR.helpdesk@incometax.gov.in

Comments are closed.